Purchasing your first home can be the largest financial decision of your life, but it can also be an exciting financial milestone. However, while a trusted realtor will offer you invaluable advice, you will still need to do a lot of work to have a good sense of a realistic budget. Only you can determine how much you can really afford, and the biggest mistake you can make will be to overlook some important details of your financial situation. Strive to be very careful, and let this list guide you towards making the right decisions.

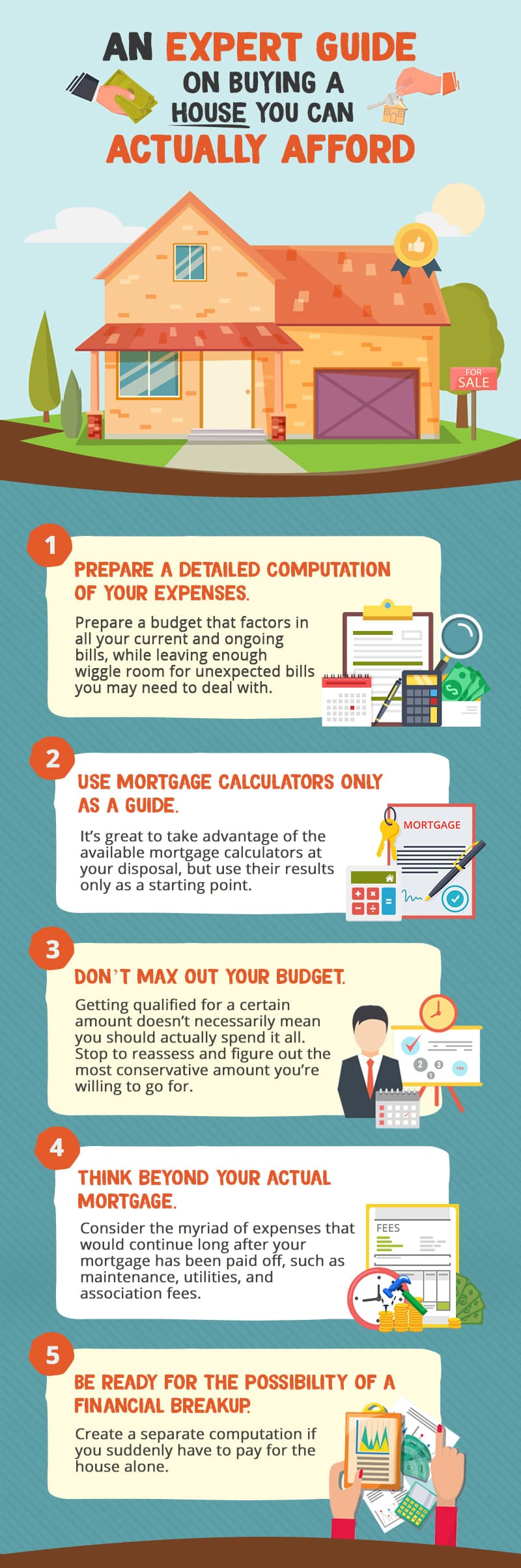

1. Prepare a detailed computation of your expenses.

Prepare a budget that factors in all your current and ongoing bills, while leaving enough wiggle room for unexpected bills you may need to deal with. An old rule you’ll be unwise to follow still is allowing yourself to buy a home that is priced two to three times your gross income. This computation doesn’t take into account your debts and monthly family expenses. Make a list of everything you pay for on a monthly basis, including credit cards, student loans, car amortizations, savings, and even date nights with your spouse. Allot a fixed budget for each so that you can have a precise idea of exactly how much would be left to spend on homeownership costs.

2. Use mortgage calculators only as a guide.

It’s great to take advantage of the available mortgage calculators at your disposal, but use these only as a starting point. Take a closer look at the results and make further computations based on the stability of your income and how personal choices in the future may affect your cash flow. Are you planning to have a baby in the next two to three years? Are you thinking of going to graduate school? These kinds of plans will have a major impact on your finances, so make accurate predictions and think as far ahead as you possibly can.

Also note that very few calculators will be thorough enough to allow a holistic look at your current financial situation, so be careful with the ones you choose to use as you may end up overestimating your financial capacity. Try slashing a good 20% off the affordability results shown by the typical online calculator, and you’ll see that this figure is a more realistic or practical amount.

Also note that very few calculators will be thorough enough to allow a holistic look at your current financial situation, so be careful with the ones you choose to use as you may end up overestimating your financial capacity. Try slashing a good 20% off the affordability results shown by the typical online calculator, and you’ll see that this figure is a more realistic or practical amount.

3. Don’t max out your budget.

Getting qualified for a certain amount doesn’t necessarily mean you should spend it all. The costs of homeownership are highly variable since property taxes and insurance costs change every year. However, most lenders will qualify you for a mortgage payment based on your dues for the current year and will leave no room for adjustments should your expenses go up in the following years. This is why it is essential to figure out the most practical way to spend the amount you’ve been approved for.

4. Think beyond your actual mortgage

Consider the myriad of expenses that would continue long after your mortgage has been paid off, such as maintenance, utilities, and association fees. Some of these fees are even likely to increase over time, so it’s best to do the math and figure out if you’ll be comfortable handling all these simultaneous expenses.

5. Be ready for the possibility of a financial breakup.

While the possibility of a breakup between you and your spouse sounds impossible at the moment, it is still advisable to cover all your bases and be comfortable with the idea of paying for the house alone. This doesn’t mean that you’re preparing for an inevitable separation – this can simply help determine whether you’ll be able to shoulder your monthly dues if your spouse suddenly loses his/her job, or if he/she cannot contribute for a particular stretch of time. This will also help you avoid taking such a risky loan.